Le mie ricette per la real estate community

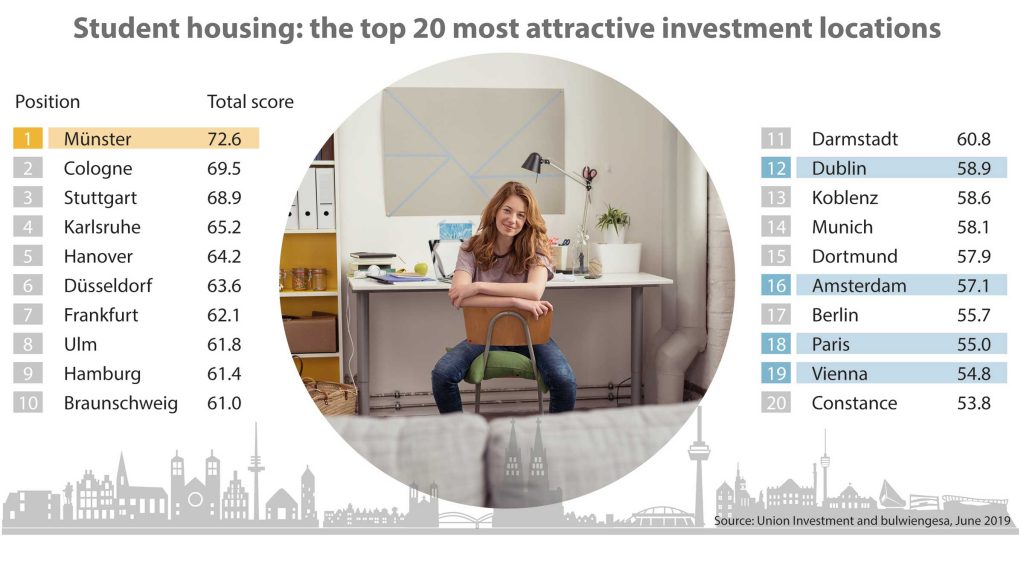

Le mie ricette per la real estate communityThe university city of Münster, with almost 60,000 students, is the most attractive location for investment in new student housing. That is the finding of a new city ranking by Union Investment and bulwiengesa, part of an in-depth study comparing supply and demand in this sector across 61 German cities using 18 different metrics. Münster is followed at the top of the ranking by Cologne, Stuttgart, Karlsruhe and Hanover. The lowest ranked city is Trier – below Kaiserslautern, Bamberg, Greifswald and Chemnitz. The study also examines four non-German cities: Dublin, Amsterdam, Paris and Vienna, all of which ranked in the top third.

“The

top 20 cities with the best conditions for investment in the student

housing sector are an interesting mix comprising all seven German Class A

cities, four major European university cities,

plus a large number of ‘hidden champions’. A strategy that focuses

exclusively on Class A cities ignores the opportunities that Münster,

Karlsruhe, Hanover, Ulm, Braunschweig, Darmstadt and Koblenz in

particular have to offer,” said Felix Embacher, Head of

Division Microliving at bulwiengesa.

According

to the study, the combined market potential for student apartments

above EUR 500 per month (all-in) in the 61 German university cities

surveyed is approximately 67,500 units. In the Class

A cities alone, there is potential demand for around 29,500 student

apartments – a 44% share of this price segment. The authors view EUR 500

per month as the threshold value for investor interest, based on

current land prices and construction costs. The potential

in this segment is particularly high in Munich and Cologne, followed by

Hamburg, Berlin and Stuttgart. The cities with the lowest potential in

this segment are Bamberg, Passau, Freiburg im Breisgau, Regensburg and

Dresden.

In

the next price segment, EUR 600–700 per month (all-in), the total

market potential is around 18,600 units. In the top price segment, above

EUR 700 per month (all-in), the estimated demand for

new student apartments is around 12,700 units.

Lack of affordable student housing concepts

“As the sector undergoes dynamic expansion of supply and increasing

professionalism through private-sector players, we should not overlook

the enormous potential of the mid-price segment,” says Henrik von

Bothmer, Investment Manager Micro-Living at Union Investment.

As

discussed in the previous year’s report by Union Investment and

bulwiengesa on Micro-Living in Europe, there is a great deal of

potential in this mid-range bracket, i.e. EUR 400–500 per month

(all-in). “The only way to provide the mid-price accommodation that the

market demands and that would be profitable for developers and

investors, especially in sought-after cities and locations, is to create

simpler housing concepts, for example with shared

kitchens or bathrooms.” Public authorities could also help plug the gap

in supply by relaxing certain building control requirements, especially

in terms of parking spaces and greater harmonisation of state building

codes.

Post-boom adjustment

The study concludes that there are attractive opportunities for

investment in new student housing across the selected university cities

during the current market cycle. However, investors should also bear in

mind that the student housing asset class emerged

during an economic boom period. “Rental expectations and appreciation

are likely to be more modest in future as the market will be unable to

maintain the price dynamics of the start-up phase.

Whatever

happens, there are some fascinating lessons in store for the student

housing asset class,” said Georg-Christian Rueb, Portfolio Manager

Micro-Living at Union Investment.

Source : Company